The Federal Reserve may possibly say normally, but in our bones, we know inflation is in this article to remain. Restaurants are having difficulties to seek the services of waiters who are holding out for larger pay grabbing a beer is starting to pinch. In the crimson-sizzling U.S. housing market, even the cheapest homes are having pricier. Very last month, producers’ selling prices in China jumped by 6.8%, so it’s just a subject of time right before the world’s major exporter brings broader inflation to the American shore.

3 p.c main inflation is not essentially undesirable news for the middle-class wallet. Annual income raises may possibly be higher and — other than cash and gold — asset benefit usually rises with the cost of living. But a man or woman has to opt for her investments additional very carefully, especially if she desires to do ambitious things, like send her kids to elite personal universities.

In a zero-inflation environment, investing was just about a no-brainer. You just place your money in the S&P 500 Index. But the calculus alterations if shopper selling prices tick up. When main inflation ranges among 3% and 6%, shares — even worth-oriented kinds — lose their attract. If history is a guide, genuine belongings — oil, base metals and agricultural solutions — will turn out to be the stars. But the center course may well have a difficult time investing in pure sources. Soon after all, you cannot stockpile corn or all-natural gasoline in your yard.

Bloomberg

Compounding the headache is soaring college or university tuition. In the very last decade, the U.S. barely professional any inflation, still by the 2019-20 academic yr, ordinary tuition, which includes home and board, at non-financial gain four-yr private universities price $48,965 a year, a 130% bounce from 20 yrs previously. So picture what the long run price tag of higher schooling will be when inflation comes into play. How should really a single commit in this new environment?

An Elite Club

Ordinary charge of attending non-public universities accounts for more than 70% of U.S. median house money, up from just more than 50% two a long time before

Resource: U.S. Census Bureau, Nationwide Centre for Training Stats

Initial, be encouraged by the Yale Design, not the 60/40 portfolio technique, which is meant to prepare for retirement. It was pioneered by David Swensen, who ran Yale University’s $31 billion endowment fund about the past three decades. In that interval, the Yale Investments Office notched an regular 12.4% annual return, and contributes to extra than a third of the school’s finances. (Swensen passed absent last week.)

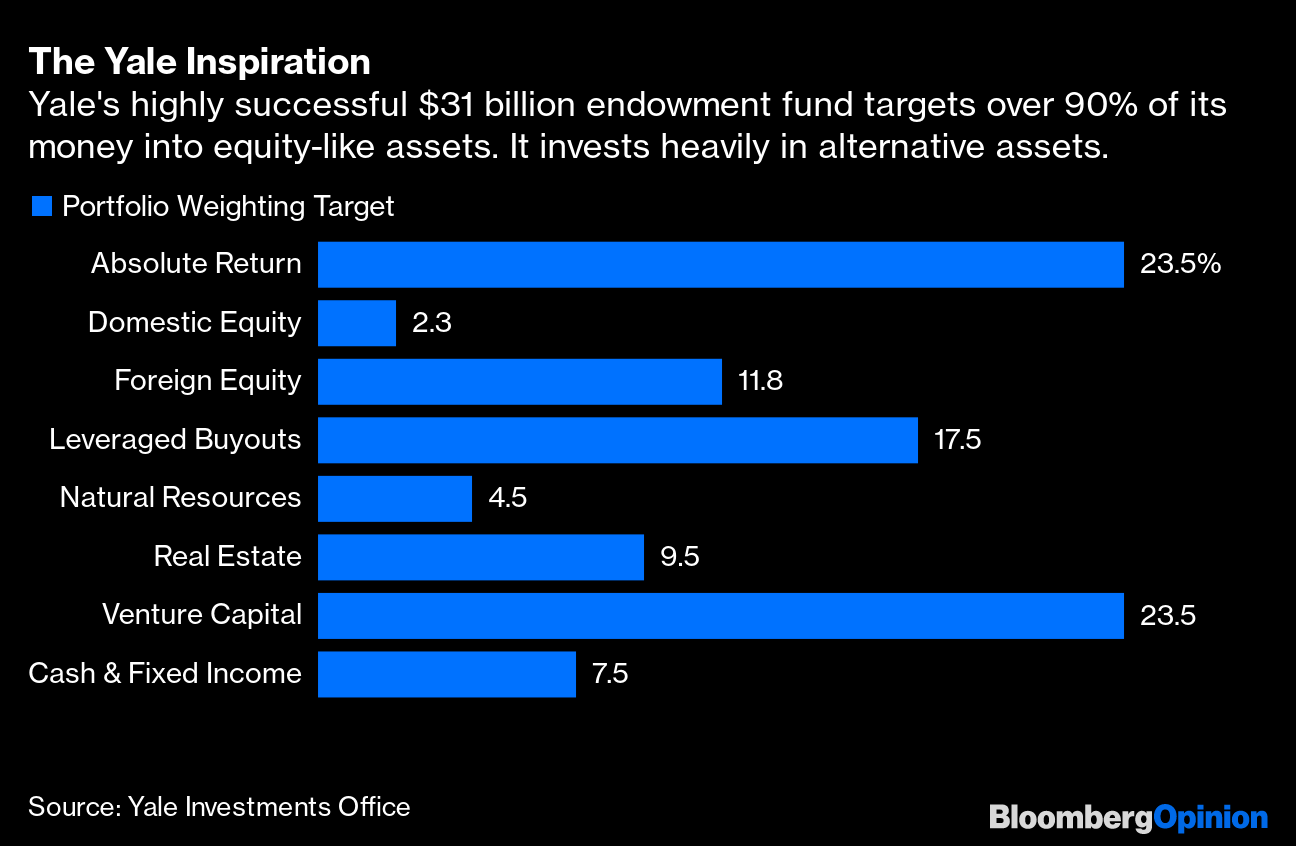

Swensen experienced to worry about the soaring cost of education — a great deal. Jogging a planet-course college is highly-priced. The general cost of operating a company aside, Yale experienced to consistently upgrade exploration amenities and lure top lecturers with good shell out. The university’s “vulnerability to inflation,” according to its latest annual report, dictated that “Yale is not especially attracted to fixed revenue property.” Relatively, far more than 90% of the endowment is qualified for investments that deliver “equity-like returns.”

Second, forget passive index investing. The Yale Model puts major aim on alternate property these kinds of as private fairness and actual estate. The fund targets 17.5% and 23.5% of its money at leverage buyouts and undertaking funds, properly higher than its peers’ typical 8.4% and 7.7% allocation. The endowment fund likes real estate, contacting it a “natural hedge” towards unanticipated inflation. The fund aims 9.5% of its cash into that sector, compared to the street’s normal 3.6% allocation.

The Yale Inspiration

Yale’s extremely successful $31 billion endowment fund targets in excess of 90% of its funds into equity-like belongings. It invests heavily in option assets.

Supply: Yale Investments Office

Are personal fairness and genuine estate superior inflation hedges? The standard wisdom is that private marketplaces will outperform publicly stated stocks due to the fact of a so-named liquidity premium. So if stocks really don’t do very well sufficient to counter the growing price of dwelling, the excess returns from the liquidity quality will give investors protection. In fact, non-public fairness has overwhelmed U.S. smaller-cap stocks by about 3% per 12 months since the mid-1990s and outperformed in about two-thirds of the decades, knowledge compiled by JPMorgan Chase & Co demonstrate.

Private fairness is a loaded man’s club. The center course, however, can however try out to faucet onto true estate, or make investments in little businesses operate by relatives and mates — which is akin to enterprise cash investing, offering a liquidity premium and advancement solutions, the bad man’s personal fairness! In an inflationary world, passive index investing is not enough to pay college costs. What you do with your wallet may possibly be the variation involving Yale and a condition school.

This column does not essentially replicate the feeling of the editorial board or Bloomberg LP and its homeowners.

To get hold of the editor liable for this tale:

Howard Chua-Eoan at hchuaeoan@bloomberg.web